The global battery energy storage systems (BESS) sector has reached a historic milestone, with total operational capacity exceeding 250 GW and overtaking pumped hydro for the first time. According to Rystad Energy, the industry saw massive growth in 2025, adding over 100 GW as it becomes a primary driver of the global energy transition. Beyond merely supporting renewables, batteries are now actively displacing gas-fired power in major markets like Australia and California. Despite potential cost fluctuations in 2026, BESS remains a highly competitive solution for modern grid stability and decarbonization.

The global energy landscape shifted significantly last year as BESS emerged as the dominant storage technology. Surpassing 250 GW in total capacity, the BESS fleet officially overtook pumped hydropower energy storage (PHES), marking a pivotal moment in the transition to renewable energy. This rapid expansion saw annual installations nearly triple compared to 2023 levels, with more than 280 GWh of capacity added in 2025 alone.

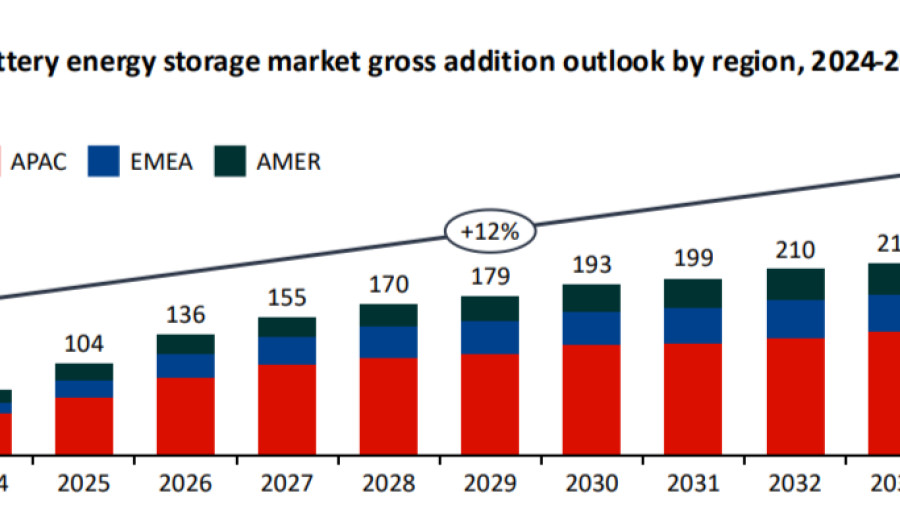

Industry analysts project that this momentum will continue into 2026, with global additions expected to reach 130 GW. While established markets like China, the United States, and Germany maintain their leadership, new regions are quickly gaining ground. Policy shifts and evolving grid requirements are driving significant project pipelines in Saudi Arabia, Italy, and Chile, signaling a broader global adoption of the technology.

One of the most notable trends is the transition of BESS from a supportive role to a primary power source. In Victoria, Australia, battery output recently exceeded gas-fired generation for the first time, a trend expected to spread to other Australian states by 2026. Similarly, in California, batteries provided over 20% of evening power during peak periods in early 2025, effectively replacing the role traditionally held by gas plants and extending the utility of solar energy into the night.

The economic landscape for storage remains favorable despite some projected headwinds. In 2025, turnkey costs in China dropped by roughly 15% to approximately $150 per kWh. However, the pace of cost reduction may slow in 2026 due to changes in Chinese export tax rebates and a recovery in lithium prices. Analysts estimate these factors could increase system costs by several percentage points in the coming year.

Nevertheless, the long-term financial outlook for BESS remains robust. Technological advancements have extended system lifespans beyond 20 years and 10,000 cycles, bringing the levelized cost of storage down to roughly $50 per MWh. In regions with high solar irradiation, co-located solar-plus-BESS installations are increasingly becoming the most cost-effective option for new power generation. Furthermore, mature markets are seeing a shift in revenue streams, with energy trading and arbitrage becoming more profitable than traditional ancillary services.