The United States energy storage sector reached an unprecedented peak in 2025, installing 18.9 GW and 51 GWh of capacity, a 52% increase over 2024 figures. Data from Wood Mackenzie’s Energy Storage Monitor highlights a massive year-end surge, with the fourth quarter alone contributing 14.8 GWh across all market segments. This rapid expansion is attributed to declining system costs, favorable federal policies, and emerging revenue streams. With a cumulative 144 GWh installed since 2019, the market is poised for significant long-term growth, with forecasts suggesting an additional 500 GWh will be deployed by 2031.

The utility-scale segment remained the primary engine of the industry, accounting for 16 GW of the total capacity added in 2025. During the final quarter, this sector deployed 4.9 GW, with activity spreading across 22 states. This geographic expansion indicates that the market is diversifying well beyond traditional strongholds like California and Texas. The growth in large-scale storage is currently supported by federal tax credits and a robust project pipeline, which includes 152 GW of categorized projects and an additional 530 GW currently sitting in interconnection queues.

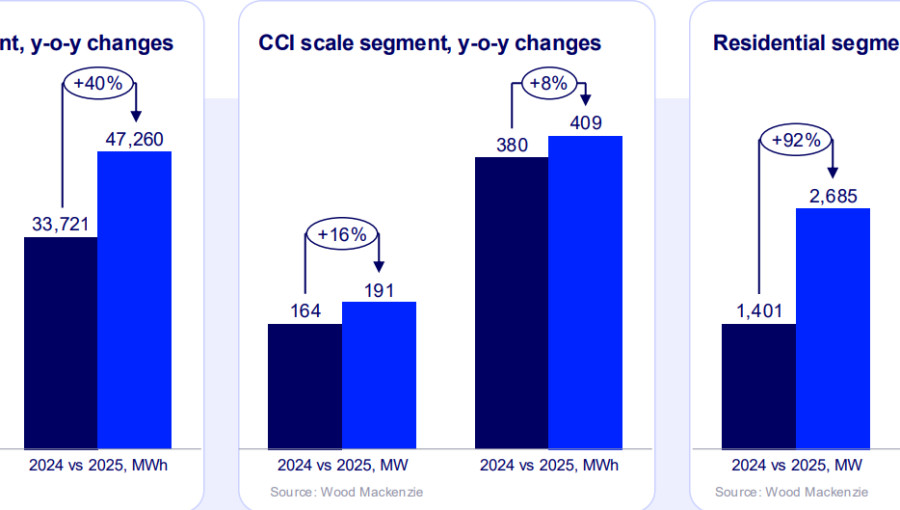

Residential storage also saw a banner year, with installations reaching 2.7 GW—a 92% jump compared to 2024. For the first time, the residential sector surpassed the 1 GWh threshold in a single quarter during the end of 2025. This spike in demand was largely driven by homeowners rushing to utilize the Section 25D Investment Tax Credit before its scheduled expiration. While California continues to lead the nation in home battery adoption, significant growth was also recorded in Puerto Rico, Texas, Arizona, and Illinois.

In the community-scale, commercial, and industrial (CCI) sector, the market grew by 16%, totaling 95.6 MW for the year. State-level policies have been instrumental in fostering community storage projects, particularly in California and New Mexico. Analysts expect the CCI segment to grow by 39% through 2030, anchored by demand in Massachusetts and New York, despite a projected temporary slowdown in 2026 due to shifting project timelines in the Midwest.

Looking toward the next decade, the industry’s trajectory remains tied to economic and regulatory variables. While the base case assumes a 250% increase in capacity by 2031 compared to the previous five-year period, trade policies and guidance regarding Foreign Entities of Concern (FEOC) could create a swing of up to 52 GW in total installations. Furthermore, the forecast assumes the Federal Reserve will lower interest rates in 2026, maintaining a range between 2.5% and 3.5% through 2030 to support continued capital investment in domestic manufacturing and large-scale infrastructure.