The European energy storage sector has reached a significant turning point, evolving from a fragmented market of experimental pilot projects into a mature, capital-intensive infrastructure industry. According to recent data, the continent’s utility-scale energy storage pipeline has surged to over 130GW across 3,000 projects in 37 countries. With roughly 19GW currently operational, the industry is preparing for a sevenfold capacity expansion over the next ten years. This transition is marked by a shift toward larger, 100+ MW projects and a growing emphasis on long-duration storage to ensure grid stability.

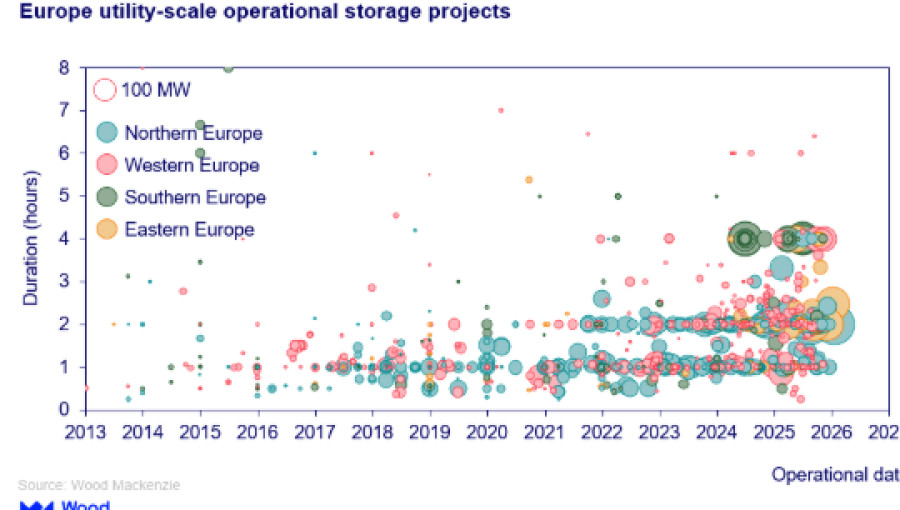

Market dynamics are shifting as the sector moves away from its niche origins. In 2025 alone, average project sizes increased by 15%, signaling that battery storage is now viewed as essential grid infrastructure rather than a secondary technology. While systems with one-to-two-hour durations still represent the majority of the market, there is an accelerating trend toward four-hour storage capacities. This evolution is driven by the urgent need to integrate renewable energy and manage the intermittent nature of wind and solar power across the European grid.

A notable change in market leadership highlights the increasing dominance of major utilities. Enel has recently overtaken Gresham House as the top asset owner of operational projects, marking the first time a traditional utility has held the lead. Enel currently manages over 1.7GW of operational capacity, primarily focused in Southern Europe. This shift reflects the impact of Italy’s capacity market and specialized auctions, moving the center of gravity away from the UK-centric portfolios that previously dominated the landscape.

The competitive environment is increasingly defined by access to significant financial backing. Leading developers are no longer independent startups but are frequently supported by massive infrastructure funds. For instance, Zenobe is backed by KKR Infrastructure Fund, while Statera and Fidra Energy are supported by EQT and EIG, respectively. This influx of institutional capital allows these firms to absorb higher risks and deliver gigawatt-scale portfolios, such as Fidra Energy’s recently announced 1,450 MW project in the UK.

Regionally, the market remains diverse in its maturity. The United Kingdom continues to lead with 7GW of operational capacity, while Germany maintains a robust pipeline supported by favorable policy frameworks. In Southern Europe, government-led auctions in Italy and Spain are driving rapid growth. Meanwhile, Eastern European nations like Poland, Bulgaria, and Romania are emerging as new hotspots, accounting for the vast majority of the pipeline in that region despite currently low operational levels.

As the industry moves forward, the ability to secure financing and navigate grid bottlenecks will determine the next generation of market leaders. With more than 70% of the European pipeline still in early-stage development, the sector is entering a phase of consolidation. Smaller, independent developers face increasing hurdles, while large-scale players with deep financial reserves are positioned to dominate the transition toward a fully decarbonized energy system.