The global energy storage sector witnessed a transformative year in 2025 as total cell shipments skyrocketed by nearly 95% to reach 612.39 GWh. According to InfoLink Consulting, the market underwent a rapid shift from a surplus of inventory to a tight supply-demand balance between the second and third quarters. While Chinese manufacturers maintain a strong lead, the industry is seeing a notable rise in momentum from mid-tier suppliers and a historic increase in demand from international markets, signaling a new phase of global expansion and technological scaling.

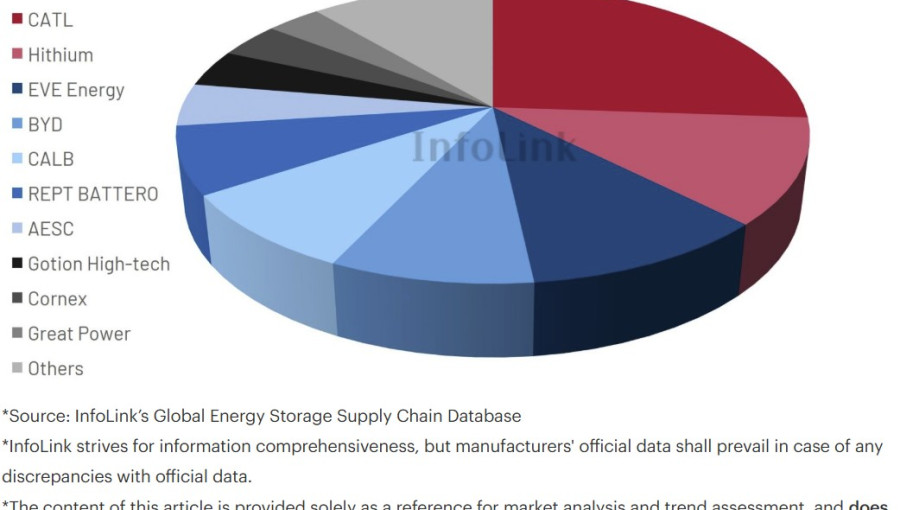

The 2025 market was defined by a volatile pricing cycle that eventually allowed manufacturers to pass higher production costs downstream to system integrators. This environment forced a diversification of supply chains as availability fluctuated quarter by quarter. Despite the volatility, the top ten suppliers controlled 88.8% of the market, with industry leaders CATL, Hithium, EVE Energy, BYD, CALB, and REPT BATTERO maintaining their dominance. Conversely, traditional Korean powerhouses LG Energy Solution and Samsung SDI saw their market shares decline, falling out of the global top ten rankings for the time being.

The utility-scale segment remained the primary driver of growth, accounting for 556.74 GWh of total shipments—a year-on-year increase of nearly 97%. Technical preferences in this sector are shifting toward larger formats, with 500 Ah+ solar cell units expected to see significant adoption by mid-2026. Specifically, 587 Ah and 588 Ah models are emerging as the preferred standard for scaling up capacity. In the small-scale storage market, which grew by over 75% to 55.65 GWh, residential demand is pivoting from 100 Ah to 314 Ah formats, which are projected to reach a 20% market penetration rate by next year.

A significant milestone was reached in the second half of 2025, as shipments to markets outside of China exceeded domestic Chinese demand for the first time on record. Non-China markets represented approximately 49% of the annual global total, reaching 299.79 GWh. CATL and BYD remained the top suppliers for these international regions, while LG Energy Solution was the sole Korean representative in the top ten for non-China shipments.

Looking ahead to 2026, analysts expect the current supply tightness to persist through the first half of the year before easing moderately. Total global shipments for 2026 are forecasted to reach 801 GWh, driven by ongoing infrastructure projects and the continued evolution of high-capacity cell technology. This growth underscores the critical role of energy storage in managing global power grids and supporting the broader transition to renewable energy.