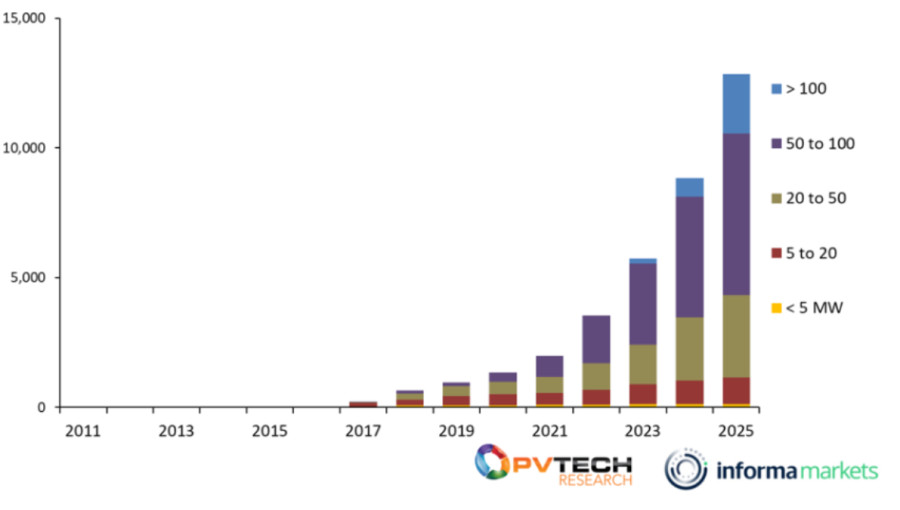

The United Kingdom’s grid-scale battery storage sector achieved a landmark performance in 2025, adding 4GWh of new capacity to reach a cumulative total of 12.9GWh. This 45% increase in operational capacity was fueled by the government’s Clean Power 2030 Action Plan, which has accelerated developer activity across the country. While the number of individual sites decreased, the market transitioned toward significantly larger installations, with the average project size growing by nearly 50%. The South East emerged as the leading region, contributing over a third of the year’s new connections.

The UK battery storage market continues its record-breaking trajectory, with new data from Solar Media Market Research revealing that 4GWh of capacity came online throughout 2025. This surge represents a 30% increase in annual additions compared to the previous year, pushing the nation’s total operational battery storage to 12.9GWh. This rapid expansion aligns with the strategic goals outlined in the late 2024 Clean Power 2030 Action Plan, which emphasized the critical need for flexible energy storage to support a decarbonized grid.

Despite the record-setting volume of capacity added, the market is showing signs of maturation. The annual growth rate moderated slightly to 45%, down from the 53% spike observed between 2023 and 2024. A notable shift in project scale defined the year; while fewer individual sites were completed, the average capacity of new projects jumped by 48% to approximately 95MWh. This trend toward utility-scale dominance is further evidenced by the fact that over 75% of the capacity added in 2025 originated from projects exceeding 50MW.

Standalone battery storage facilities remain the preferred configuration for developers, accounting for 61% of operational projects. These independent sites typically offer higher capacities compared to co-located assets, which share infrastructure with renewable energy sources. Geographically, the South East of England solidified its position as the industry’s hub. The region saw more than 1.4GWh across 10 sites go live in 2025 alone, bringing its cumulative operational capacity to over 3.2GWh.

The sector’s expansion comes amid a complex financial landscape. Revenue generation for battery energy storage systems remains volatile, particularly within ancillary service markets, and shifting government incentives continue to challenge long-term forecasting. Nevertheless, the combination of falling global battery prices and sustained investor interest suggests the market is entering a new phase of industrial-scale development. Industry analysts suggest the slight dip in growth rate is not a sign of a slowdown, but rather a reflection of the time required to bring increasingly massive and complex energy projects to completion.